Impact of Brexit on Forest Products Industry

The results of the UK referendum to leave the EU created widespread uncertainty in global financial markets; the S&P 500 fell 3.59% in the U.S., the FTSE 100 fell 3.15% in Britain, and the DAX index fell 6.82% in Germany. These bearish reactions reflect larger concerns that may contribute to reduced growth of the UK economy including increased uncertainty about future levels of household income, deteriorating terms of trade, and a discouragement to invest among UK firms.

While much attention has been placed on projecting the potential effect of Brexit on UK income, little is known about how this may impact the forest products industry. Wood products are normal goods, such that declines in national income negatively affect consumption. Therefore, declining consumption and eroding terms of trade will likely have an effect on the wood products industry within the UK; an industry with a net trade deficit in forest products of USD$9.0 billion in 2015.

While many believe Brexit will negatively impact the British economy, the magnitude of this effect remains unclear. A number of sources have provided short- and long-term forecasts of the effect of Brexit on the UK’s GDP with great speculation surrounding the UK’s ability to negotiate trade agreements. For the purposes of our study, the projected economic effects of Brexit were grouped into two categories; an optimistic scenario and a pessimistic scenario. The optimistic scenario assumes that the UK and the EU will continue to enjoy free trade and that Brexit does not create additional tariff barriers. The pessimistic scenario assumes that the UK fails to negotiate a new trade agreement with the EU, leading to increased tariffs on imports, higher non-tariff barriers to trade (i.e. changing regulations, border controls), and minimal integration between the UK and EU in future trade policy.

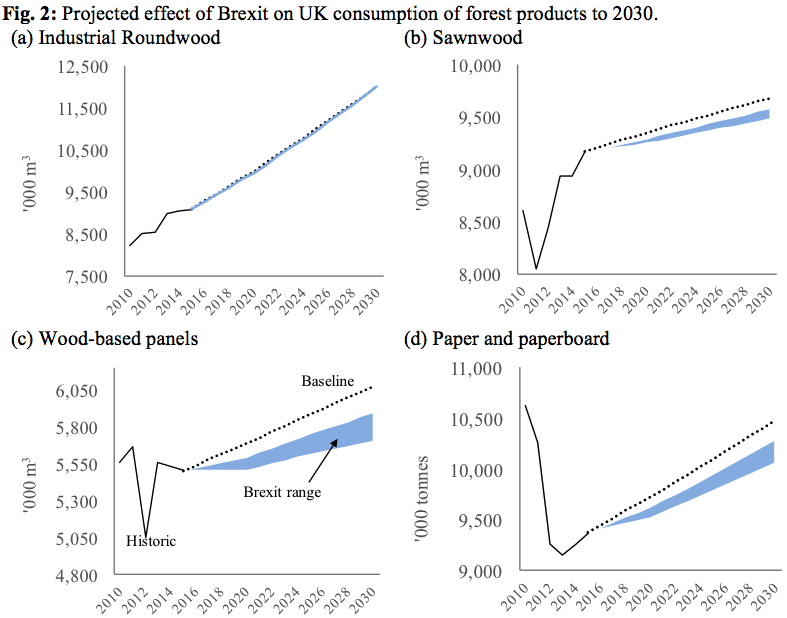

These scenarios were then simulated with the Global Forest Products Model to project the consequences for the forest industries in the UK and abroad. According to the results, Brexit caused a sustained modest decline in UK demand for wood products through 2030. The consumption of sawnwood in Britain was 1.0% to 2.1% lower by 2030, 2.9% to 6.1% lower for wood-based panels, and 1.9% to 4.1% lower for paper and paperboard. With Brexit, the UK net trade deficit in sawnwood decreased by 4.8% to 9.9% by 2030, 4.4% to 9.1% for wood-based panel, and 5.5% to 10.8% for paper and paperboard. The effects on industrial roundwood consumption and production within the UK were negligible. Both scenarios had a modest adverse effect on the global market for wood products, while the consequences of Brexit were mostly within Europe and driven predominantly by reduced consumption within the UK itself. While the effect was greater under the pessimistic scenario, the overall impact on the global wood products industry was small, and it had no discernable effect on prices.

Still, the extent to which these factors play out in the coming years remains, for the most part, unknown, and depends on a number of factors; some of which are outlined below.

First, the cost of capital may rise in the short run, as the uncertainty created through the UK’s departure from the EU calls for a higher risk premium on lending. As a result, firms will face a more difficult time acquiring capital, which will discourage investment.

Second, Brexit uncertainty may encourage the sale of UK assets, putting downward pressure on the pound. One consequence would be higher import costs, leading to further inflation. The degree to which the rise in inflation is passed through to consumers will drive reductions in consumption patterns, and the degree to which profit margins are squeezed will determine the degree of job losses within the UK. Meanwhile, the depreciation of the pound will cause imports to decline allowing the external balance to improve, mitigating the depth of the GDP contraction.

Third, the ability for the UK to negotiate trade deals with important trading partners will drive the magnitude of the economic effect of Brexit, and thus the impact on the forest products industry. There are many possible scenarios for the UK’s future position, ranging from preserving its existing trade relationship with the EU to a failure to reach agreements and a reversion to World Trade Organization tariffs.

Finally, the degree in which Britain continues to pursue EU mandated policies will likely play a large role in determining the impact of Brexit on the forest products industry. For example, the UK currently subsidizes energy produced from biomass in order to comply with EU’s legislated renewable energy targets set out for 2020 and 2030. As a result, the United Kingdom has emerged as one of the world’s largest consumers of wood pellets, with 6.8 million m3 consumed 2015; 93% of this consumption is imported from outside its borders, primarily from North America.

In the end, the changes to income levels associated with the UK’s departure from the EU will likely be too insignificant to cause any substantial disruptions in wood product markets within Britain, or surrounding regions.

This article was posted in Faculty Research and tagged Brexit, Forest Products, Trade.